Breaking Borders: Asia's Cross-Border Payment Revolution

Imagine this: A tourist in Bali pays for her villa using a QR code linked to her Singapore bank. Seconds later, the payment reflects in the local merchant’s account—minimal fees, zero intermediary delays. Nearby, a Malaysian importer settles a Thai supplier’s invoice in local currencies, bypassing costly USD conversions. These aren’t futuristic scenarios—they’re Asia’s rapidly evolving cross-border payment ecosystem in action.

Cross-border payments in Asia are undergoing a seismic transformation, driven by innovation, regional collaboration, and the sheer scale of trade and remittance flows. This article explores the mechanics behind this shift, the latest innovations, and the inefficiencies being tackled.

What Are Cross-Border Regional Payments?

Cross-border regional payments enable transactions between countries in a specific region, such as ASEAN, while sidestepping traditional global systems reliant on the USD or intermediary banks. These systems emphasize:

• Interoperability: Linking domestic payment networks seamlessly.

• Cost Efficiency: Cutting conversion and banking fees.

• Real-Time Capabilities: Delivering near-instant settlements.

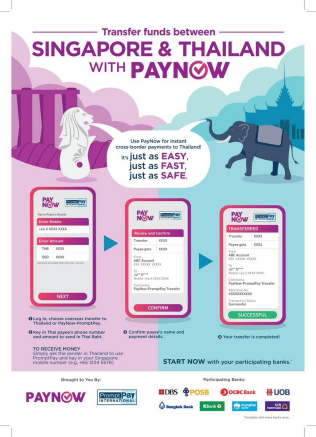

A notable example is the integration of Thailand’s PromptPay and Singapore’s PayNow, enabling cross-border transfers via QR codes or phone numbers without high forex costs.

Key Innovations Shaping the Ecosystem

1. B2B Buy Now/Pay Later (BNPL): Flexible, short-term credit with low interest rates is transforming business financing.

2. Embedded Finance: Financial services embedded in platforms enhance customer experiences, offering contextual payments and lending.

3. Central Bank Digital Currencies (CBDCs): Pilots like Thailand and Hong Kong's mBridge enable direct cross-border settlements.

4. Interoperable QR Codes: Shared standards streamline transactions, eliminating the need for proprietary systems.

5. Real-Time Payments: Instant settlements improve liquidity and boost regional trade efficiency.

6. Sustainable Payments: Eco-friendly solutions, like digital payments, align with consumer demand for green practices.

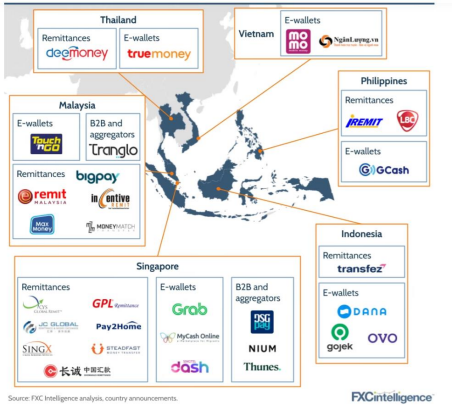

Successful Models Across Asia

1. ASEAN Payment Connectivity

The ASEAN region leads with QR code-based systems. Key milestones include:

• Thailand-Malaysia Link: Consumers use PromptPay and DuitNow for direct, local-currency payments via QR codes.

• Indonesia-Singapore Integration: BI-FAST and PayNow facilitate real-time cross-border transactions, expanding digital connectivity.

2. China’s Cross-Border Interbank Payment System (CIPS)

China’s CIPS reduces reliance on SWIFT, enabling faster, cheaper RMB trade settlements. In 2022, CIPS handled over $100 billion in transactions, streamlining payments for ASEAN-China trade.

3. India’s UPI Expansion

India’s Unified Payments Interface (UPI) revolutionizes domestic payments and is scaling globally. Its integration with Singapore’s PayNow showcases real-time international payment potential.

Also read: What is UPI, what it is not?

The QR Code Revolution

QR codes are at the heart of Asia’s payment transformation. Cost-effective and hardware-free, they enable businesses to accept payments instantly. Applications range from retail and e-commerce to public transport and cross-border trade.

• Domestic Use: Retail, utilities, and bill payments.

• Cross-Border Payments: Automatic currency conversions make travel and global shopping seamless.

• Public Mobility: Ride-hailing and parking systems embrace QR-based payments.

By 2025, global QR code payments are expected to exceed $3 trillion, driving financial inclusion and redefining commerce.

The ASEAN Payment Market: A Snapshot

• Trade Volume: ASEAN trade grew from $871 billion in 2003 to $3.56 trillion in 2023, with intra-ASEAN trade accounting for 22%.

• Remittances: South Asia’s remittances reached $186 billion in 2023, underscoring the demand for efficient payment systems.

• E-Commerce Growth: Cross-border e-commerce logistics in Asia are projected to hit $213 billion by 2030.

The rise of digital payments is a backbone for this growth, with ASEAN’s digital economy forecast to reach $1 trillion by 2025.

Bottlenecks in Current Systems

Despite advancements, inefficiencies remain:

• High Costs: Cross-border fees range from 3–10%, particularly in remittance corridors.

• Settlement Delays: Traditional systems like SWIFT can take days, disrupting business cash flow.

• Fragmented Regulations: Varied standards across ASEAN hinder interoperability. • Exchange Rate Risks: Reliance on the USD exposes smaller economies to volatility.

Emerging Alternatives

1. Blockchain Solutions

Platforms like RippleNet eliminate intermediaries, enabling secure, real-time, and low-cost payments.

2. Central Bank Digital Currencies (CBDCs)

Projects like Singapore’s Ubin and Thailand-Hong Kong’s mBridge enable cross-border transactions without intermediary banks.

3. Digital Wallet Ecosystems

GrabPay and GCash are expanding functionality to cater to ASEAN’s gig economy, enhancing cross border accessibility.

4. Interlinked Payment Systems

Systems like PayNow and PromptPay lead ASEAN’s charge toward real-time, regional payment interoperability.

The Road Ahead

Asia’s cross-border payment transformation is inevitable. As trade, remittances, and e-commerce demand efficiency, innovations like blockchain, CBDCs, and interoperable QR systems are setting the stage for faster, cheaper, and inclusive payments. The region’s payment systems are evolving into global benchmarks, breaking barriers and connecting economies.

The question remains: can policymakers and private players sustain the momentum to fully realize this vision?