What UPI Is—and What It Isn’t: The Future of Global Payments?

India’s Unified Payments Interface (UPI) has revolutionised the payments landscape, not just in India but increasingly on a global scale. Six years since its launch, UPI has evolved from being a domestic enabler of cashless payments to a symbol of India’s technological prowess, with growing global recognition. Yet, as its adoption skyrockets, there remain misconceptions about what UPI truly is—and what it’s not.

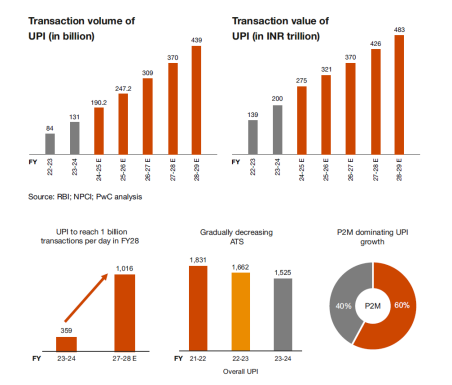

With over 131 billion transactions in FY 2023-24 and projections to hit 439 billion by FY 2028-29, UPI has become synonymous with India’s digital transformation. But beyond these staggering numbers lies a deeper narrative of financial inclusion, cross-border cooperation, and the future of global payments.

For exclusive insights on investment trends, geopolitics, family office relevant themes and wealth preservation, follow Vedas Group Asia’s LinkedIn page

Source: PwC report on UPI

*ATS = Average ticket size

*P2M = Person to Merchant Transaction

1INR = 0.012 USD

For exclusive insights on investment trends, geopolitics, family office relevant themes and wealth preservation, follow Vedas Group Asia’s LinkedIn page

Section 1: UPI—A PAYMENT BEHEMOTH

UPI is a real-time payment system that allows instant peer-to-peer (P2P) and peer-to-merchant (P2M) transactions by linking multiple bank accounts through a single mobile app.

It's built on an open-source model, making it scalable and interoperable with a wide array of financial service providers. Yet, it’s not just a technological solution—UPI’s greatest achievement is accessibility. From urban tech-savvy professionals to rural users with basic mobile phones, UPI bridges all demographics.

Success Stories & Scale

In FY 2023-24, UPI accounted for over 80% of India’s digital retail transactions. What’s driving this?

The key lies in the simplicity and trust that UPI has built. Unlike traditional banking apps, UPI has zero downtime, works across multiple platforms, and has grown to accommodate newer use cases like bill payments, online purchases, and even microloans.

Five years ago, UPI was handling a few million transactions. Today, it processes over 1 billion transactions daily. And this is just the beginning. With innovations like UPI 2.0 enabling overdraft facilities and UPI Autopay for recurring transactions, the ecosystem is growing beyond basic transfers.

Key Data Point 1: A 57% year-on-year growth in transaction volume shows no signs of slowing down. Over 131 billion transactions were processed in FY 2023-24, and this is expected to triple by 2029.

Key Data Point 2: More than 80% of India's retail digital payments are conducted through UPI, and this share is projected to rise to 91% by 2029.

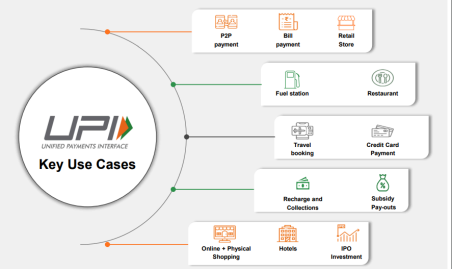

Use Cases Driving Growth

The largest driver for UPI’s growth has been its ability to serve a variety of needs across the economic spectrum. Whether it’s a street vendor accepting payments via QR code, a middle-class family paying their monthly utility bills, or a startup enabling salary disbursements—UPI has it all covered.

1. Micro-Payments: Financial Inclusion

UPI’s zero-cost structure is a game-changer for rural India, enabling the unbanked to access the formal financial system. It’s now the go-to platform for direct government transfers and micro-transactions, bringing millions into the digital economy.

2. Merchant Payments: QR Code Revolution

For small businesses, UPI’s instant settlement and QR code payments have reshaped operations. With over 352 million QR codes deployed, even street vendors can access fast, cashless transactions, especially in tier 2 and 3 cities.

3. Recurring and Bill Payments

For exclusive insights on investment trends, geopolitics, family office relevant themes and wealth preservation, follow Vedas Group Asia’s LinkedIn page

UPI’s Autopay feature simplifies recurring transactions for utilities, subscriptions, and insurance premiums. Whether it’s paying an electricity bill or renewing a Netflix subscription, UPI’s seamless automation ensures users never miss a payment.

4. Peer-to-Peer (P2P) Payments

From splitting dinner bills to quick loan repayments, UPI’s ease of use for P2P transactions has made it the default for casual, everyday transfers. It’s instant, fee-free, and accessible to all.

5. Corporate Disbursements

UPI has become a reliable tool for salary payments, especially for gig workers. Platforms like Swiggy and Uber use UPI to ensure their workers are paid immediately after tasks are completed, eliminating payroll delays.

6. E-Commerce Integration

UPI’s integration with platforms like Amazon and Flipkart has streamlined the checkout experience, reducing cart abandonment. Its instant payment system is transforming online retail, while integration with digital wallets widens its appeal.

7. Cross-Border Payments

UPI’s next frontier is cross-border remittances. With India processing over $125 billion in remittances in 2023, UPI’s global partnerships aim to make transfers faster and cheaper for the Indian diaspora.

8. B2B Payments

Though UPI began in retail, its future lies in B2B payments. UPI’s real-time settlement and invoicing capabilities could streamline corporate payments and improve supply chain management.

Source: National Payment Corporation of India 2023 report

Key Data Point 3: The QR code network now boasts over 352 million deployments, driving small and medium business participation in digital payments.

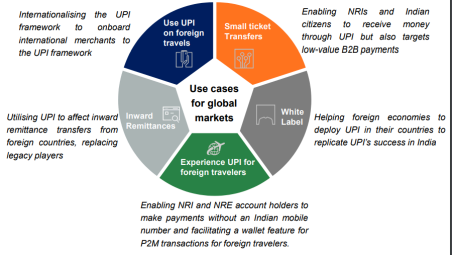

SECTION 2: UPI’s GLOBAL FUTURE

As impressive as UPI's domestic footprint is, its ambitions stretch far beyond India’s borders. The Indian government, along with the National Payments Corporation of India (NPCI), has been actively working to export the UPI model to other countries. Several nations have already adopted or are exploring UPI-based systems for their local economies, which could position India as a global leader in digital payments infrastructure.

Global Expansion: The International Playbook

Cross-border payments are often plagued by high fees and long delays, creating friction for businesses and individuals. UPI's real-time, low-cost architecture has sparked interest globally. Countries like Singapore, Bhutan, and the UAE have already integrated UPI into their payment ecosystems. Moreover, partnerships with global financial institutions are in place to enable seamless remittances between India and countries like Nepal, Malaysia, and Oman.

Key Data Point 4: In 2023 the global remittances to India reached $125 billion, equivalent to 3.4% of the country’s GDP. With the aim to internationalise UPI, it is on the way to become a critical tool for cross-border payments.

Source: National Payment Corporation of India 2023 report

SECTION 3: CHALLENGES AHEAD FOR GLOBAL ADOPTION

However, global adoption isn’t without its challenges. Different regulatory environments, varying customer behaviours, and existing financial infrastructures can make integrating UPI tricky.

What UPI Is Not

It’s crucial to clarify what UPI isn’t. UPI is not a universal replacement for all payment methods, nor is it an answer to all financial system challenges. It doesn’t solve the issue of financial literacy, nor is it a panacea for economies with heavily entrenched payment ecosystems.

UPI complements the current financial systems, offering faster, cheaper, and more secure alternatives for small and medium-sized transactions. Its success has not cannibalized other digital payment methods but rather accelerated overall digital adoption.

What UPI can do—and what it is doing—is reimagining how everyday transactions happen globally. It’s becoming a vital layer in cross-border fintech collaborations and enabling frictionless remittances across nations.

Key Data Point 5: By 2029, UPI is projected to handle 1 billion transactions daily, cementing its place as one of the largest and most efficient payment systems in the world.

Challenges

Despite its successes, UPI faces challenges that could impede growth:

For exclusive insights on investment trends, geopolitics, family office relevant themes and wealth preservation, follow Vedas Group Asia’s LinkedIn page

Infrastructure Limitations: Current infrastructure may struggle under anticipated spikes in transaction volume without significant upgrades.

Global Competition: As other countries develop their own digital payment systems, UPI must remain competitive through continuous innovation.

SECTION 4: THE FUTURE: UPI 3.0 & BEYOND

The future of UPI lies in expanding its capabilities across credit, biometrics, and international partnerships. The integration of biometrics for authentication, expected to replace the PIN-based system, promises to elevate both security and user experience. This shift could streamline payments with facial recognition or fingerprint verification, making fraud even more difficult.

On the global front, UPI One World, a prepaid wallet designed for international travelers, is already in motion, allowing visitors from G20 nations to use UPI seamlessly in India. This move highlights UPI’s ambition to set global standards for payments.

But its greatest untapped potential might lie in B2B payments. While UPI has conquered retail transactions, its robust infrastructure could also support B2B, domestic and cross-border business transactions. This shift could revolutionise international trade by cutting out intermediaries and reducing costs, offering businesses real-time payments at a fraction of today’s fees.

Far from just a technological innovation, UPI is redefining financial access globally. As India pushes UPI to new heights, the system is poised to become a blueprint for countries aiming to democratise finance. The question now is not if UPI will transform global payments, but how quickly it will.