Are Payments the new vista for Financial Inclusion

Financial inclusion remains a pressing global issue, with 1.5 billion people in emerging markets lacking access to formal savings or credit. Reliant on cash, many turn to informal lenders, leaving themselves financially vulnerable and isolated.

However, digital payments are transforming this landscape. Mobile wallets, digital banking, and blockchain are creating pathways to the formal financial system, offering affordable, secure services and enabling access to underserved populations.

DIGITAL PAYMENTS LEADING A GROWTH STORY

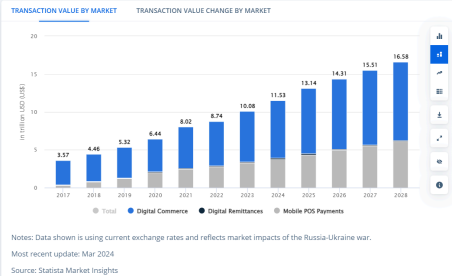

According to Statista, digital payment transactions are projected to reach $11.53 trillion in 2024, with an annual growth rate (CAGR) of 9.52% through 2028, hitting $16.59 trillion by 2028. This expansion is not just about convenience—it's fostering sustainability for financial service providers and driving long-term inclusion.

For exclusive insights on investment trends, geopolitics, family office relevant themes and wealth preservation, follow Vedas Group Asia’s LinkedIn page

The numbers tell the story

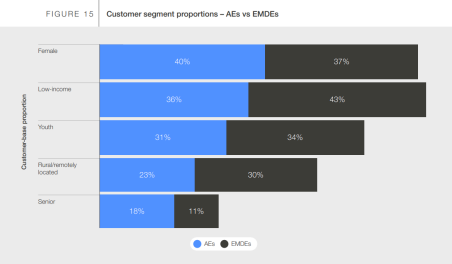

According to the World Economic Forum, globally, underserved customer segments—including women, low-income, and rural populations—comprise a large share of fintech users, contributing substantial transaction volumes.

This trend is consistent across both Advanced Economies (AEs) and Emerging Markets and Developing Economies (EMDEs), with fintech platforms increasingly serving those left behind by

For exclusive insights on investment trends, geopolitics, family office relevant themes and wealth preservation, follow Vedas Group Asia’s LinkedIn page traditional financial institutions.

TECHNOLOGY AT PLAY: FROM CASH TO DIGITAL

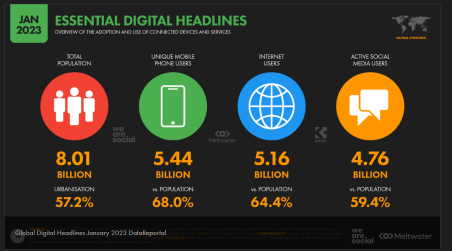

The rapid adoption of smartphones has been a catalyst for financial inclusion, with 68% of the global population now owning a mobile device, according to GSMA.

For exclusive insights on investment trends, geopolitics, family office relevant themes and wealth preservation, follow Vedas Group Asia’s LinkedIn page

This shift is particularly impactful in regions like sub-Saharan Africa and Southeast Asia, where traditional banking infrastructure is limited. Mobile networks and digital wallets, such as GCash in the Philippines and Alipay in China, are bridging this gap, allowing millions to access financial services remotely. Some other successful examples include the M-Pesa platform in Kenya and Paytm in India.

Technology is driving down transaction costs, making financial services more accessible, unlocking opportunities for underserved populations to participate in the financial system and pushing inclusivity to new levels.

The future of financial inclusion therefore deeply hinges on continued tech advancements, that transform how financial services are delivered, offering low-cost, scalable solutions to reach remote and marginalized populations at unprecedented speed.

THE ROLE OF GOVERNMENT AND REGULATIONS

Governments around the world are increasingly using digital payment systems to enhance financial inclusion. India's Unified Payments Interface (UPI), launched in 2016, processes over 9 billion transactions monthly (NPCI), making financial services easily accessible for millions. Brazil's Pix is similarly transforming payments in Latin America, with Colombia following suit.

A global initiative, Project Nexus, led by the Bank for International Settlements (BIS) and central banks from Malaysia, the Philippines, Singapore, Thailand, and India, aims to connect domestic instant payment systems across borders. This system is designed to lower cross-border transaction costs and foster greater financial inclusivity.

Governments across the globe are also introducing favorable regulatory environments to foster innovation in digital payments. The UK’s Open Banking Initiative is a key example, allowing third-party financial providers to access consumer banking data, which encourages competition and improves financial services. Similarly, Kenya's mobile money platform M-Pesa benefited from regulatory flexibility, enabling widespread adoption and financial inclusion.

Public private partnerships in this area are also growing. Many governments are collaborating with the private sector to expand digital payment systems. For example, in Indonesia, the government partnered with private telecom companies to launch QRIS, a unified QR code system, making digital payments more accessible to micro, small, and medium enterprises (MSMEs). Financial literacy campaigns is another area where governments and regulators are playing a big role. Across Asia, initiatives are being taken to educate people in the remote regions on the advantages of digital payments, helping them transition to this method versus cash.

For exclusive insights on investment trends, geopolitics, family office relevant themes and wealth preservation, follow Vedas Group Asia’s LinkedIn page

McKinsey estimates that digital financial services could boost economies by up to USD 3.7 trillion by 2025. Governments are critical to scaling these innovations and ensuring their sustainability.